Just when you thought the end of the year couldn’t get any more intriguing, a significant options expiration is ready to shake things up in this highly leveraged market.

Options are derivative contracts that give the buyer the right to buy or sell the underlying asset at a pre-set price at a later date. A call option gives the right to buy and a put option gives the right to sell.

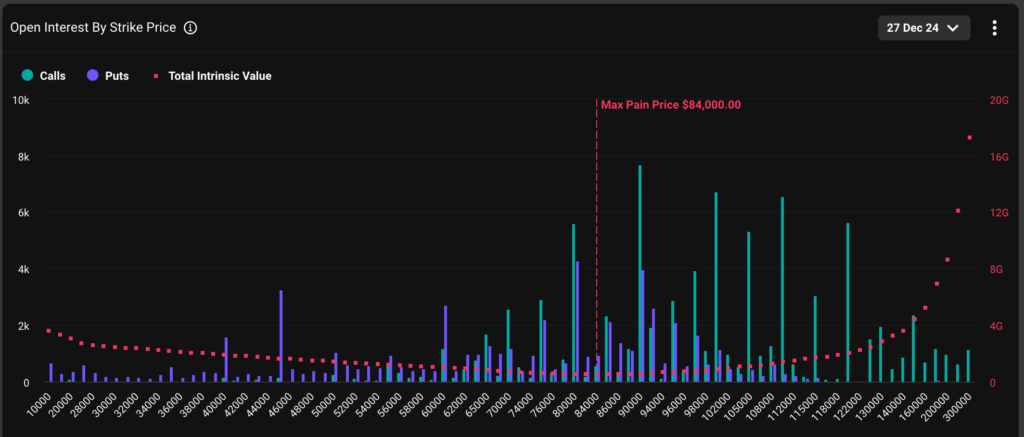

On Friday at 8:00 UTC, 146,000 bitcoin options contracts, valued at almost $14 billion and sized at one BTC each, will expire on the Deribit cryptocurrency exchange. The face amount represents 44% of the total open interest for all BTC options at different maturities, marking the largest expiration event ever seen on Deribit.

ETH options worth $3.84 billion will also expire. ETH has fallen almost 12% to $3,400 since the Federal Reserve meeting. Deribit represents over 80% of the global crypto options market.

Important OI to expire ITM

At the time of writing, it appeared that Friday’s deal would see $4 billion in BTC options, representing 28% of the total $14 billion open interest, expire “in-the-money (ITM) “, generating a profit for buyers. These positions can be squared off or rolled over (rolled over) to the next expiration, which could cause market volatility.

“I suspect a good amount of open interest in BTC and ETH will shift to the January 31 and March 28 expirations as the closest liquidity anchors at the start of the new year,” said Simranjeet Singh, portfolio manager and trader at GSR. .

It’s also worth noting that the put open interest ratio for Friday’s expiration is 0.69, meaning there are seven puts open for every 10 calls outstanding. A relatively higher open interest in call options, which provides an asymmetric advantage to the buyer, indicates that leverage is biased to the upside.

The problem, however, is that BTC’s bullish momentum has lost steam since last Wednesday’s Fed decision, where Chairman Jerome Powell ruled out potential Fed purchases of the cryptocurrency and signaled fewer rate cuts for 2025. .

Since then, BTC has fallen more than 10% to $95,000, according to data from CoinDesk indices.

This means that traders with leveraged bullish bets risk larger losses. If they decide to throw in the towel and exit their positions, it could lead to more volatility.

“Previously dominant bullish momentum has stalled, leaving the market highly leveraged to the upside. This positioning increases the risk of a rapid snowball effect if a significant bearish move occurs,” Deribit CEO Luuk told CoinDesk. Strijers.

“All eyes are on this expiration as it has the potential to shape the narrative heading into the new year,” Strijers added.

Directional uncertainty persists

Key options-based metrics show that there is a notable lack of clarity in the market regarding potential price movements as the record expiration approaches.

“The long-awaited annual expiry is about to conclude a banner year for bulls. However, directional uncertainty remains, highlighted by higher volatility (vol-of-vol),” Strijers said.

Volatility volatility (vol-of-vol) is a measure of fluctuations in the volatility of an asset. In other words, it measures how much volatility or the degree of price turbulence fluctuates in the asset itself. If the volatility of an asset changes significantly over time, it has a high vol-of-vol.

A high vol-of-vol generally means greater sensitivity to economic news and data, leading to rapid changes in asset prices, requiring aggressive adjustment of positions and hedging.

The market is more bearish on ETH

The current price of expiring options reveals a more bearish outlook for ETH relative to BTC.

“Comparing the vol smiles of the [Friday’s] expiration between today and yesterday, we see that the BTC smile is almost not moving, while the implied ETH call volume has decreased significantly,” Andrew Melville, research analyst at Block Scholes.

A volatility smile is a graphical representation of the implied volatility of options with the same expiration date but different strike prices. The drop in implied volatility of ETH calls means lower demand for bullish bets, indicating a moderate outlook for the native Ethereum token.

This is also evident in options bias, which measures how much investors are willing to pay for calls that offer asymmetric upside potential versus puts.

“After more than a week of worse spot performance, the ETH Buy and Sell Bias Index is more strongly bearish (2.06% in favor of puts compared to a more neutral 1.64% towards purchase options for BTC)”, Melville noted.

“Overall, the year-end positioning reflects a moderately less bullish picture than what we saw in December, but still more marked for ETH than for BTC,” Melville added.