The value in dollars blocked in open XRP options listed in Delibit is rapidly rising to a record since the high implicit volatility of Token attracts performance hunters.

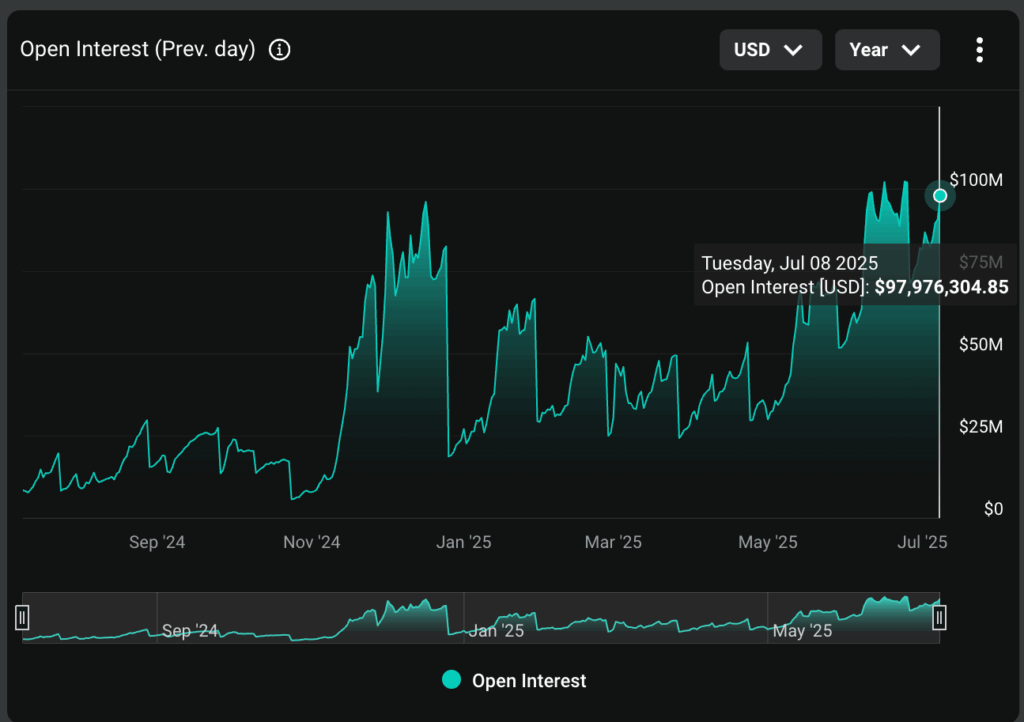

The so -called open interest (I heard) It has increased to almost $ 98 million from $ 71 million from the quarterly expiration of June 27, a solid increase of 38% in two weeks. Now he is approaching the June 24 record, $ 102.3 million, according to Data Source Deribit Metrics. In terms of contract, the OI has increased by 26% to 42,414. (The contract multiplier for XRP in Deribit is 1,000 xRp).

Behind the increase is the implicit volatility of Token, a measure of the expected price changes during a specific period. XRP is higher than Bitcoin

Ether and Solana, according to Lin Chen, head of business development of Asia of Deribit.

“XRP has delivered an annual yield of more than 300% in the last 12 months,” Chen told Coindesk. “His options have also gained significant popularity, reflected in the greatest implicit volatility among the main tokens, indicating a strong demand for investors.”

One Way that merchants are getting profits is selling puts in cash, Chen said. Writing a sales option, agreeing to buy the asset at an established price, is similar to selling insurance against price falls in exchange for a premium, which represents the sales of the seller.

The operators generally write options against holdings in the spot market or in a “cash assured” way when the implicit volatility is high. The greater the volatility, the more expensive the options and vice versa. The version insured by the cash implies keeping enough stable to ensure that the underlying asset can be purchased if prices slide and buyer Put decides to exercise their right to sell the asset at the predetermined price.

Risk reversions are biased bundles

At the time of writing, the risk reversions of 25 De-Delta were positive, indicating a bias towards the purchase options or the bullish bets, according to data tracked by Amberdata.

The risk reversion of 25 De-Delta is a strategy that includes a long sale position and a short purchase option (or vice versa) With a 25%delta, which means that both options are relatively far from the current price of the underlying asset market.

The price of risk reversions in tenors helps identify the feeling of the market, with positive values that represent a relative wealth of negative calls and values that indicate a downward bias. At the time of publication, XRP risk reversions in the short term and those linked to August and September expirations were positive.

In addition, more than 30 million calls were open, exceeding 11.92 million positions, giving a ratio of 0.39, also a sign of upward feeling in the market.

Discharge of responsibility: Parts of this article were generated with the assistance of AI tools and reviewed by our editorial team to guarantee the precision and compliance with our standards. For more information, see Coindesk’s complete policy.